7月8-9日,“2023 面板数据与时间序列计量经济学前沿国际研讨会——致礼萧政教授对中国计量经济学的杰出贡献” 在太阳成集团tyc7111cc经济楼成功举办。

本次国际研讨会由太阳成集团tyc7111cc邹至庄经济研究院、NSFC“计量建模与经济政策研究”基础科学中心主办,中国科学院预测科学研究中心、《计量经济学报》协办。

汇名家思想、聚学者观点,会议吸引到来自63所高校的160多位学者参加,他们分别来自中国、美国、新加坡、澳大利亚、加拿大、英国、韩国、荷兰、丹麦等多个国家。在两天的议程中,主办方共安排了8场主题演讲,16位主题演讲嘉宾带来最前沿的计量经济学研究成果;另有23个平行分会场中共80位报告人带来论文报告。研讨会在为现代计量经济学研究前沿的讨论和交流创造良好的环境的同时,致礼萧政教授对计量经济学理论及其应用所做出的杰出贡献。

除了火热的现场讨论之外,本次国际研讨会的线上直播也吸引了许多关注。会议在太阳成集团tyc7111cc经济学科视频号和学说平台进行了全程直播,其中仅主会场8日上午开幕式及主题演讲的直播观看量就达到1.5万人次,其余场次的主题演讲观看人次也都近万;各分会场的论文报告同样收获不俗点击率,直播观看最高达4000余人次。

Keynote Session I

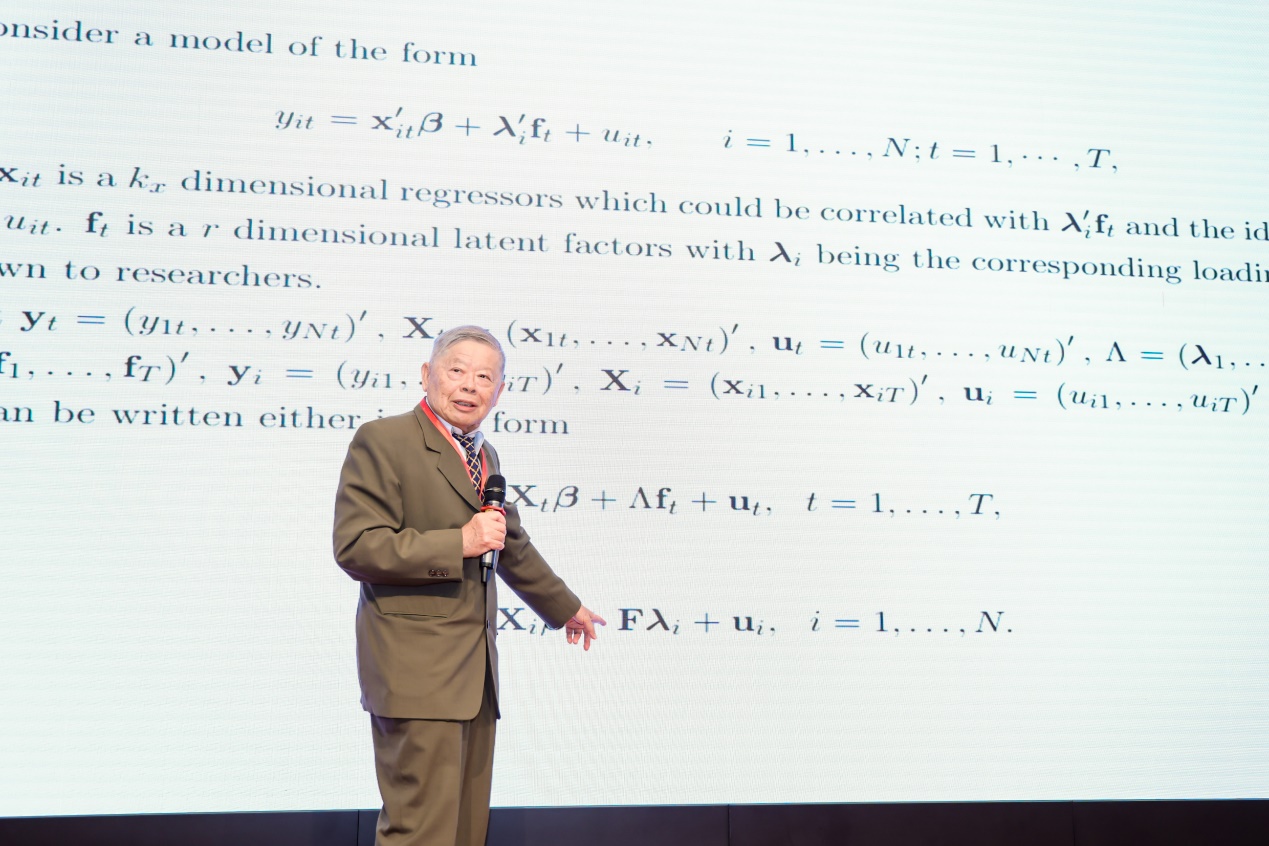

Cheng Hsiao, University of Southern California

Panel Interactive Effects Models with Endogenous Regressors

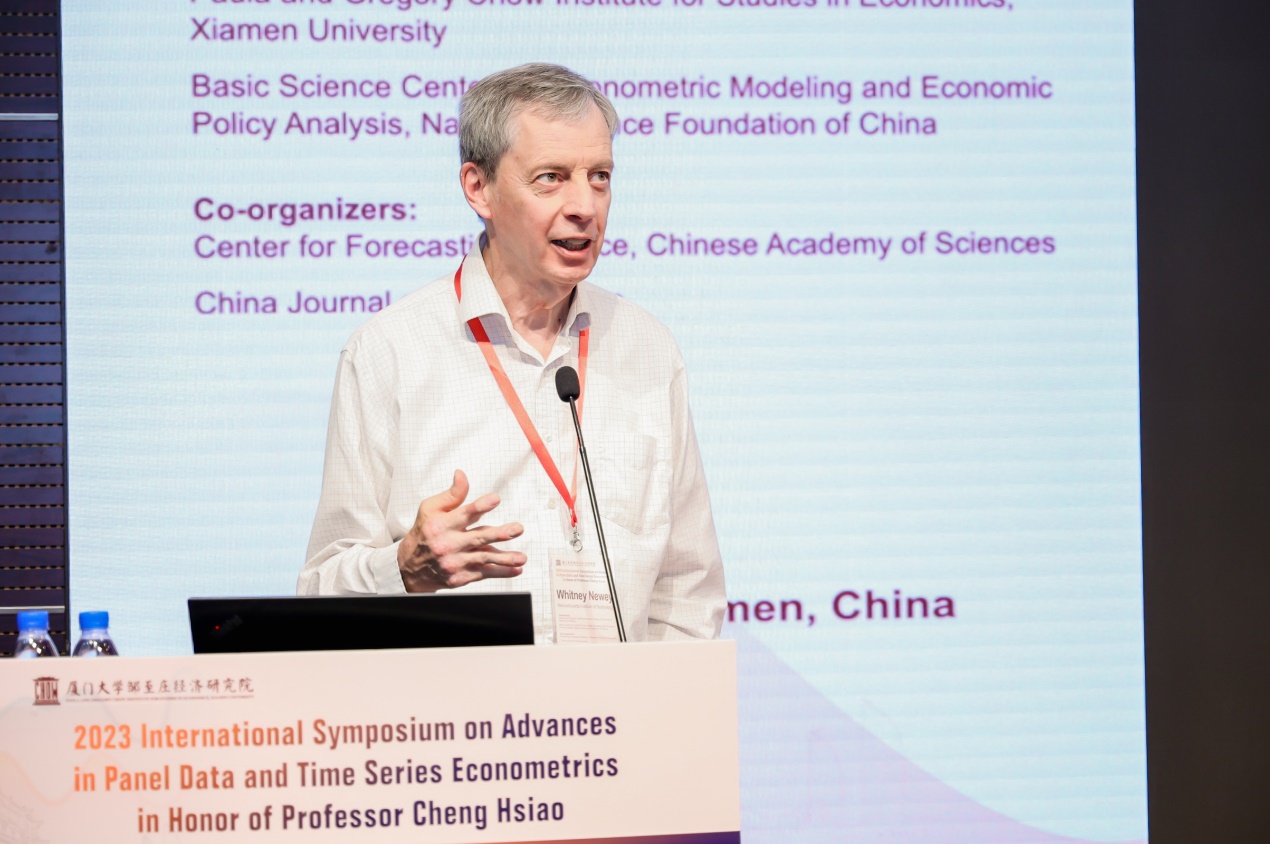

Whitney Newey, Massachusetts Institute of Technology

Linear Estimation of Structural Effects for Nonseparable Panel Models

Keynote Session II

Lung-Fei Lee, Shanghai University of Finance and Economics

ML Estimation of a SAR Hurdle Model for Origin-Destination Flow Variables

Dennis Lin, Purdue University

Data is Power

Keynote Session III

Wai Keung Li, The Education University of Hong Kong

Time Series Models for Realized Covariance Matrices Based on the Matrix-F Distribution

Yahong Zhou, Shanghai University of Finance and Economics

Identifying Group Clustered Patterns in Quantile Regression

Keynote Session IV

Shiyi Chen, Fudan University

Combating Cross-Border Externalities

Weiguo Wang, Dongbei University of Finance and Economics

数字金融发展与消费侧碳排放--来自家庭层面的微观证据

Keynote Session V

Chunrong Ai, The Chinese University of Hong Kong, Shenzhen

A Unified Estimation of General Panel Data Treatment Models

Liangjun Su, Tsinghua University

Three-Dimensional Heterogeneous Panel Data Models with Multi-level Interactive Fixed Effects

Keynote Session VI

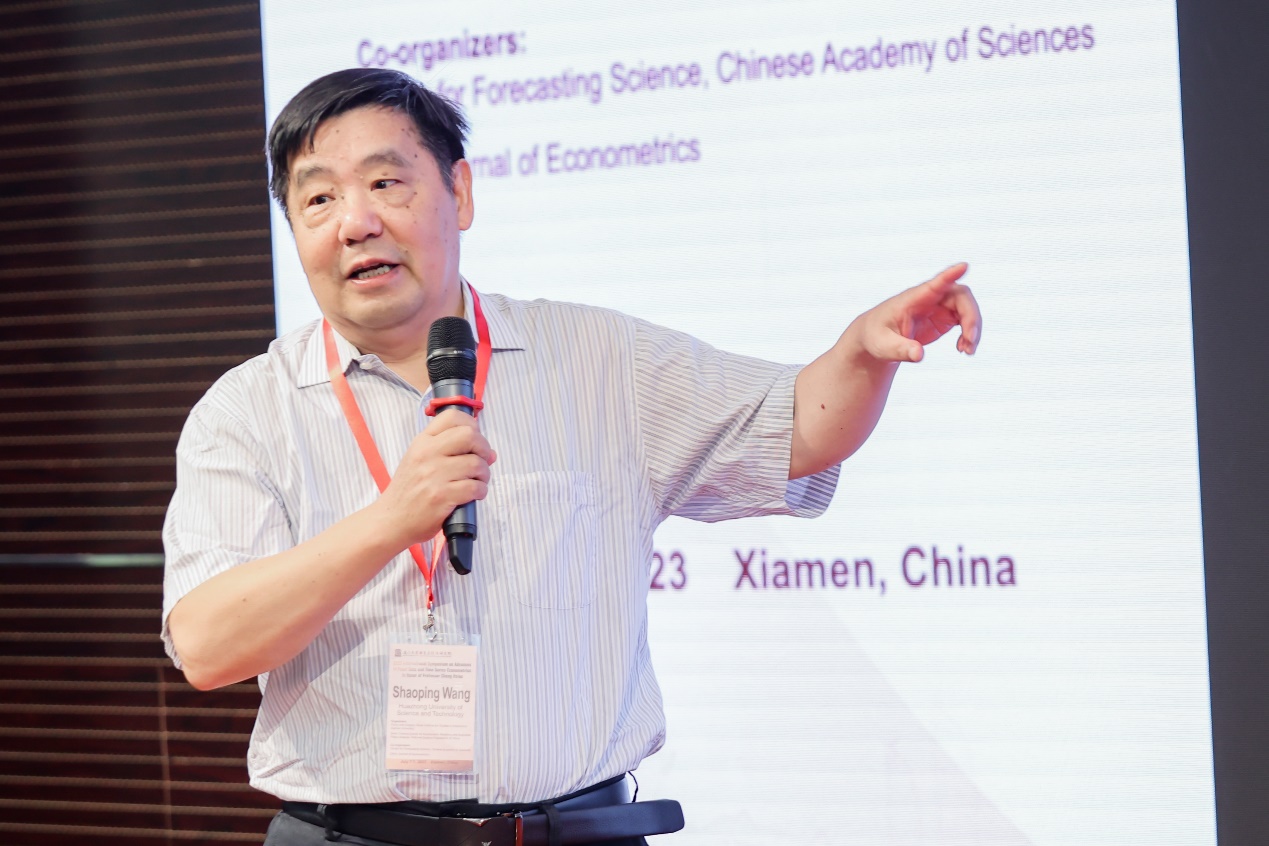

Shaoping Wang, Huazhong University of Science and Technology

A Bubble or a Quadratic Trend? Evidence from a New Test for Unit Roots with a Partial Quadratic Trend

Pingfang Zhu, Shanghai Academy of Social Sciences

Research on the Incentive Effect of the R&D Expense Deduction Policy: Evidence from Non-state-owned High Tech Industries

Keynote Session VII

Kunpeng Li, Capital University of Economics and Business

Control Interactive Fixed effects with Diversified Projections

Shiqing Ling, Hong Kong University of Science and Technology

Testing for Change-points in Heavy-tailed Time Series--A Trimmed CUSUM Approach

Keynote Session VIII

Yongmiao Hong, University of Chinese Academy of Sciences & Xiamen University

Forecasting Inflation Rates Using a Large Panel of Individual Stock Prices

Zhijie Xiao, Boston College

Quantile Control via Random Forest

(太阳成集团tyc7111cc 周梦娜)